If you've ever borrowed money or opened a credit card, chances are, you've paid interest to your lender. Banks are quick to brag about record low interest rates, but does that really matter when you compare it to the cost of a house you want to buy? In this lesson, we're going to talk about what interest rates are and what they actually mean, and why it's so important to understand them before borrowing money.

What Is an Interest Rate?

What does an interest rate mean?

to save your progress

Do you have any credit cards? If you do, what is the interest rate for your card?

What is interest?

When we choose to use a service, we usually pay a fee. Borrowing money is no exception. Banks and other lenders don't let people borrow money out of the goodness of their hearts - they do it to make a profit. And since loans can be for different amounts, purposes, and lengths of time, it doesn't make sense to charge a set fee to borrow money. Instead, lenders charge borrowers an interest rate, or a percentage of the loan amount, calculated over the length of the loan. Interest rates can vary depending on a borrower's history of repayment, loan amount, and time, but understanding what an interest rate means is key to understanding how much you will end up paying for your loan.

Vocabulary

To understand the terms of a loan, we must first understand all of the vocabulary banks and lenders use to describe them. Here are a few standard terms that come up when talking about loans.

Principal: The amount of money initially borrowed from a lender

- Example: Lucas takes out a loan for $500 at 6% interest compounded monthly. The principal for his loan is $500.

Interest Rate: The percentage of the principal a lender charges a borrower

- Example: Lucas takes out a loan for $500 at 6% interest compounded monthly. Lucas's interest rate is 6%.

Annual Percentage Rate (APR): Sometimes, you'll see an interest rate followed by the acronym "APR." It's safe to assume that most interest rates are annual rates, or rates charged over the period of a year, but some lenders add APR just to clarify.

- Example: A credit card has an interest rate of 12% APR. This means that the 12% interest is spread out over a full year.

Compounded: While the interest rate tells us what percentage of our loan the lender will charge us, the compounding frequency tells us how often the interest is calculated. Loans can be compounded annually, monthly, quarterly, biweekly, or even daily, but the more frequently the interest is compounded, the more we pay over time.

- Example: Lucas takes out a loan for $500 at 6% interest compounded monthly. This means his loan calculates and adds his interest to his principal every month, or twelve times a year.

The bank offers you a car loan for $15000 at 4% interest. What is your principal? What is your interest rate?

How do you calculate interest?

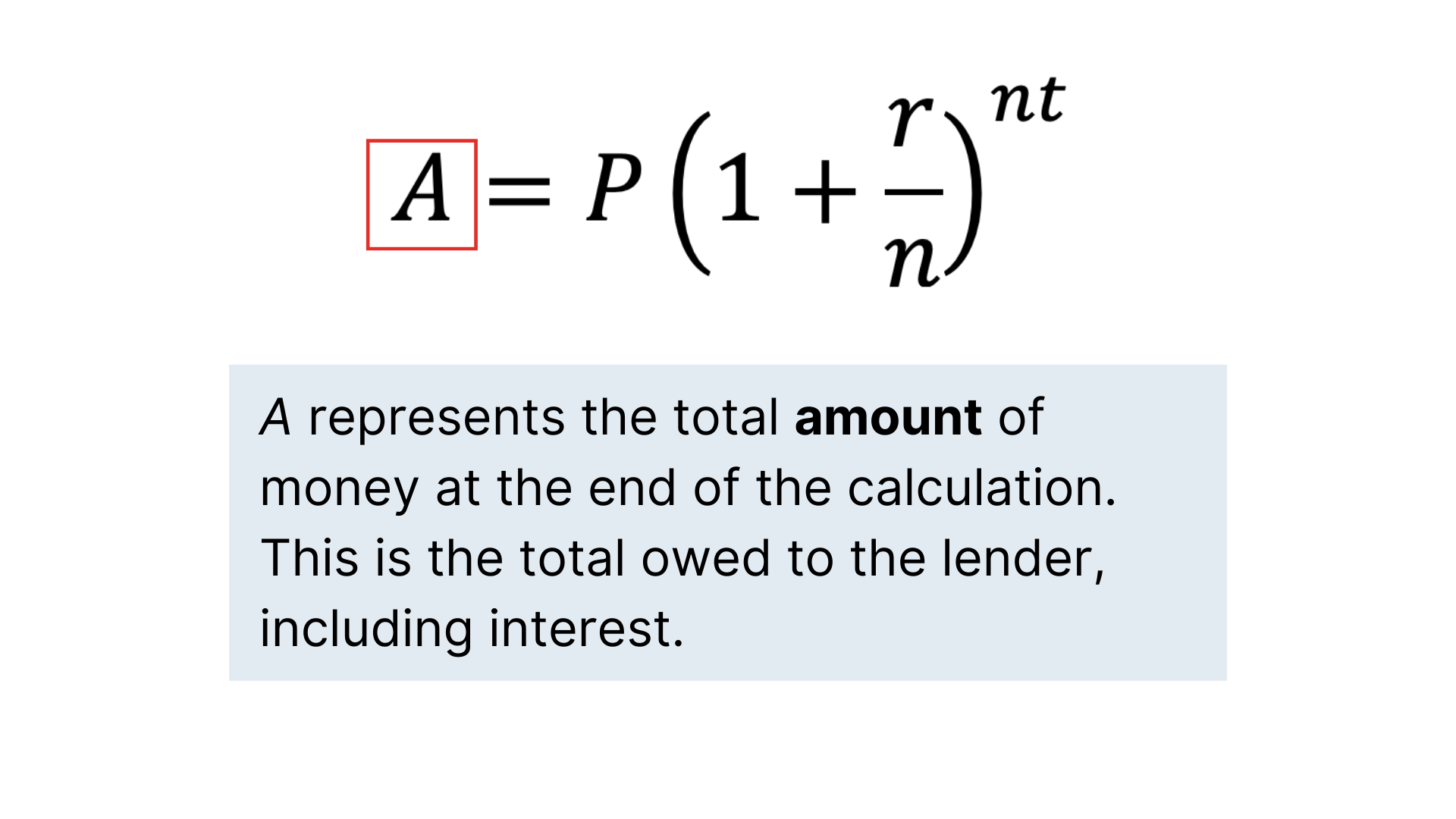

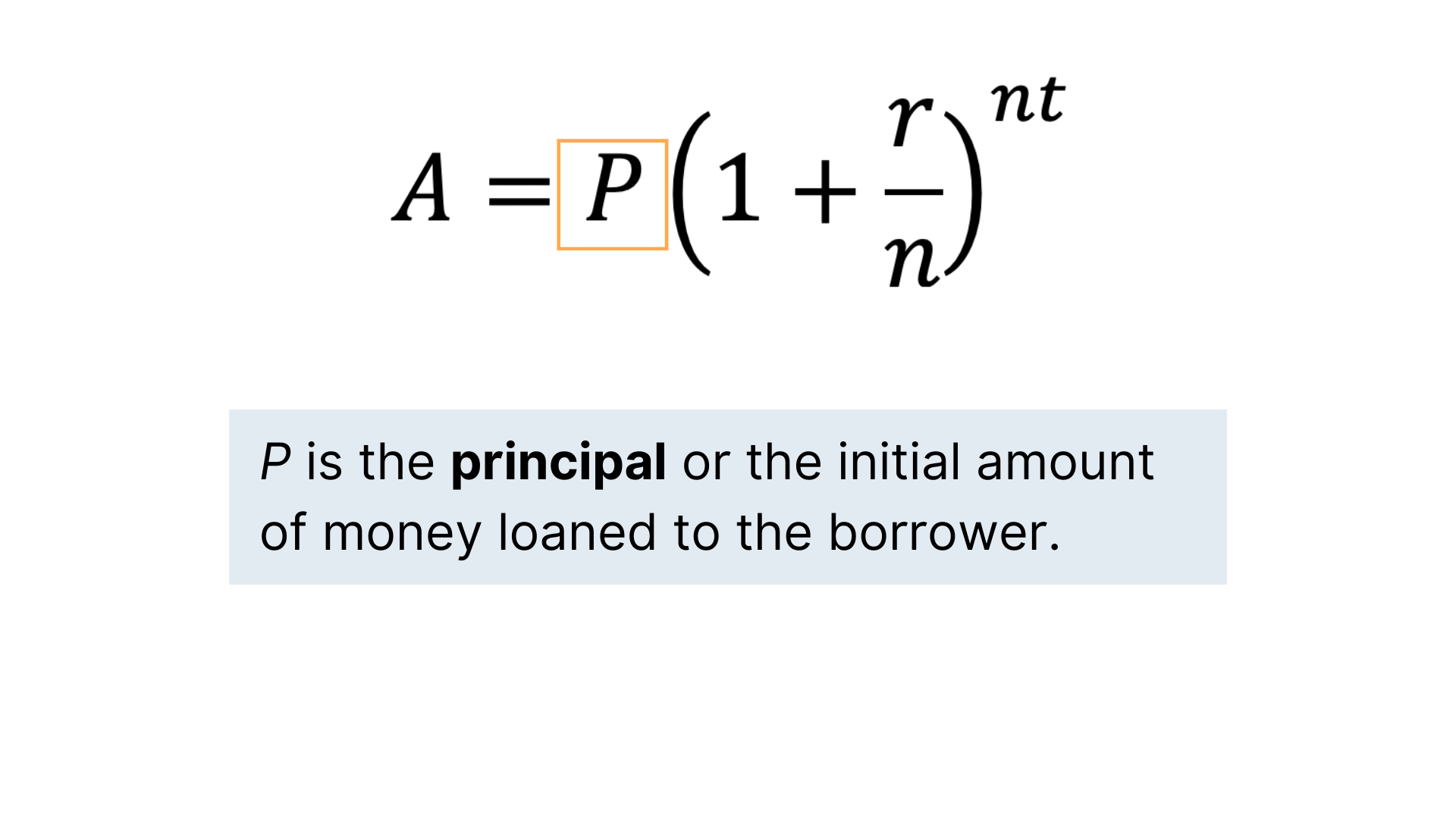

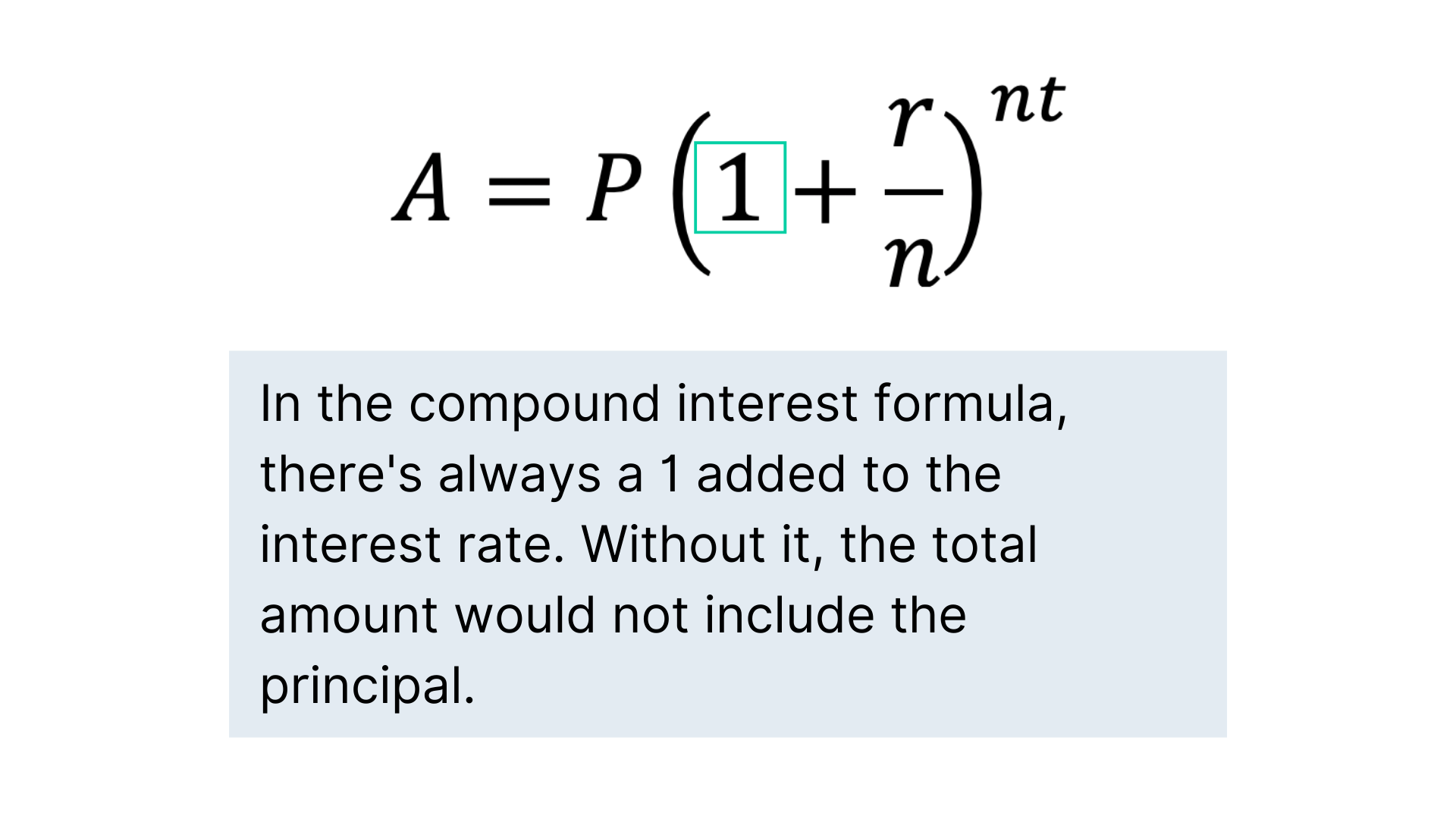

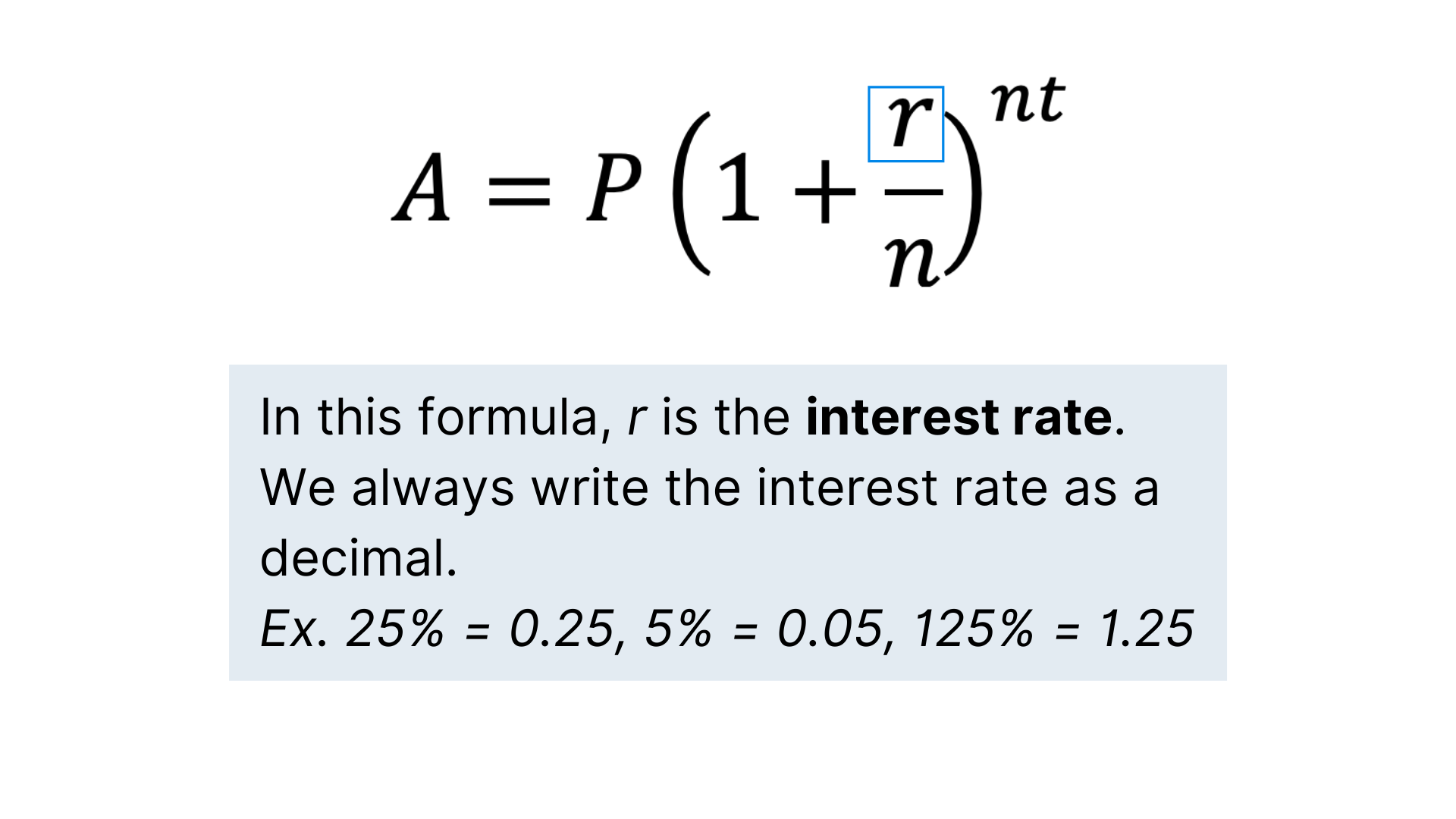

When we borrow money, it's rare that we have to calculate the interest on our own loans; lenders will almost always do their own calculations. But, while this can sometimes feel like magic, interest is actually calculated with a formula you can use on your own. Flip through the slides below to learn about the parts of the compound interest formula.

Here's an example of how this formula can be used.

The Desmos scientific calculator is a great tool for calculating compound interest. If you need help using it, you can find a quick tutorial here.

This equation has a lot of parts, and it can seem overwhelming. If you're feeling overwhelmed by the formula, take a deep breath. It's important to understand the different parts and why they're important, but know that your bank will always calculate the interest you owe for you.

Does interest really matter?

Key Factors

Interest rates on credit cards often look very different from interest rates on mortgages. Interest rates always affect how much money you'll pay, but here are a few factors that allow them to make an even bigger difference.

1. Amount Borrowed

When you look at interest rates, you might notice that smaller loan amounts tend to have higher interest rates and larger loan amounts tend to have lower interest rates. Because the amount of interest owed depends on the amount of principal borrowed, even a low interest rate can cost you a lot of money on a major purchase, like a house.

Let's look at the monthly payments for a $200,000 house with a 30-year fixed-rate mortgage.

- 3% interest: $843 per month

- 4% interest: $955 per month

- 5% interest: $1074 per month

The interest rate makes a big difference in how much you pay. An increase of just 1% can mean you owe over $100 more each month, or over $36,000 over the life of the loan!

2. Length of Loan

The amount of total interest you pay depends on the principal, but also on the length of the loan. Since you're charged your interest rate every year you owe money, each additional year adds to your total. Mortgages are often offered for 15- or 30-year terms, and car loans are generally for 3 to 6 years (36 to 60 months). Your monthly payments will be higher for a shorter-term loan, but you'll pay less in the long run.

Consider a $15,000 car loan with a 5% interest rate.

- 36 months: $450/month; $16,184 total

- 48 months: $345/month; $16,581 total

- 60 months: $283/month; $16,984 total

If you pay your car loan over 60 months, you end up paying about $800 more than you would have paid for a 36-month loan. That doesn't mean you should never take out a 60-month loan - the payments over 36 months are much higher - but the lower payments do come at a cost over time. This cost is even more significant with a higher interest rate, so beware of high interest rates for longer-term loans.

Your friend is buying a house and tells you they found a loan they could pay over 60 years. They're excited because their monthly payments are very low and they'll save tons of money. What advice do you have for them before they agree to the loan?

Predatory Interest

Sometimes, we borrow money to make big purchases we might not be able to afford all at once, like a house or a new car. Usually, we put a lot of time into researching these big purchases, and banks will compete with each other to win your loan with the best interest rate. But other times, we borrow money because we have to. Even when we budget carefully, surprise costs like medical bills, car repairs, and special occasions can make it hard to make ends meet. In these emergency situations, predatory lenders, like those that advertise payday loans, take advantage of people who need money quickly.

Payday loans charge an average interest rate of 391% APR. The loans are generally for smaller amounts from $100-$1000, but since 80% of borrowers don't pay back their loan within the two-week window, they end up costing much more.

Let's look at a $300 loan with a 390% interest rate compounded every 14 days.

- If you paid your loan back after two weeks, you'd pay $345 total in principal and interest.

- If you paid your loan back after four weeks, you'd pay $397 total in principal and interest.

- If you paid your loan back after six weeks, you'd pay $456 total in principal and interest.

Compare that to a $300 charge on a credit card with a 20% interest rate compounded daily.

- If you paid off your card after two weeks, you'd pay $302 total in principal and interest.

- If you paid off your card after four weeks, you'd pay $305 total in principal and interest.

- If you paid off your card after six weeks, you'd pay $307 total in principal and interest.

The interest rate makes a huge difference! In just six weeks, you owe nearly $150 more with the high-interest loan. That's a lot of money to borrow $300.

Your friend had a minor accident that left her with a $100 medical bill she could not afford. She tells you she found a payday lender who could get her the $100 the same day without a credit check. What advice do you have for her before she takes out the loan?

to save your progress